Renewable energy for sustainable development in India: current status, future prospects, challenges, employment, and investment opportunities

The primary objective for deploying renewable energy in India is to advance economic development, improve energy security, improve access to energy, and mitigate climate change. Sustainable development is possible by use of sustainable energy and by ensuring access to affordable, reliable, sustainable, and modern energy for citizens. Strong government support and the increasingly opportune economic situation have pushed India to be one of the top leaders in the world’s most attractive renewable energy markets. The government has designed policies, programs, and a liberal environment to attract foreign investments to ramp up the country in the renewable energy market at a rapid rate. It is anticipated that the renewable energy sector can create a large number of domestic jobs over the following years. This paper aims to present significant achievements, prospects, projections, generation of electricity, as well as challenges and investment and employment opportunities due to the development of renewable energy in India. In this review, we have identified the various obstacles faced by the renewable sector. The recommendations based on the review outcomes will provide useful information for policymakers, innovators, project developers, investors, industries, associated stakeholders and departments, researchers, and scientists.

Introduction

The sources of electricity production such as coal, oil, and natural gas have contributed to one-third of global greenhouse gas emissions. It is essential to raise the standard of living by providing cleaner and more reliable electricity [1]. India has an increasing energy demand to fulfill the economic development plans that are being implemented. The provision of increasing quanta of energy is a vital pre-requisite for the economic growth of a country [2]. The National Electricity Plan [NEP] [3] framed by the Ministry of Power (MoP) has developed a 10-year detailed action plan with the objective to provide electricity across the country, and has prepared a further plan to ensure that power is supplied to the citizens efficiently and at a reasonable cost. According to the World Resource Institute Report 2017 [4, 5], India is responsible for nearly 6.65% of total global carbon emissions, ranked fourth next to China (26.83%), the USA (14.36%), and the EU (9.66%). Climate change might also change the ecological balance in the world. Intended Nationally Determined Contributions (INDCs) have been submitted to the United Nations Framework Convention on Climate Change (UNFCCC) and the Paris Agreement. The latter has hoped to achieve the goal of limiting the rise in global temperature to well below 2 °C [6, 7]. According to a World Energy Council [8] prediction, global electricity demand will peak in 2030. India is one of the largest coal consumers in the world and imports costly fossil fuel [8]. Close to 74% of the energy demand is supplied by coal and oil. According to a report from the Center for monitoring Indian economy, the country imported 171 million tons of coal in 2013–2014, 215 million tons in 2014–2015, 207 million tons in 2015–2016, 195 million tons in 2016–2017, and 213 million tons in 2017–2018 [9]. Therefore, there is an urgent need to find alternate sources for generating electricity.

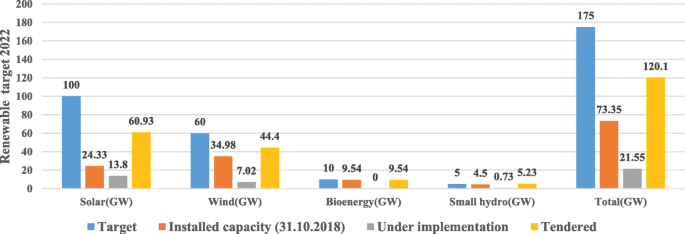

In this way, the country will have a rapid and global transition to renewable energy technologies to achieve sustainable growth and avoid catastrophic climate change. Renewable energy sources play a vital role in securing sustainable energy with lower emissions [10]. It is already accepted that renewable energy technologies might significantly cover the electricity demand and reduce emissions. In recent years, the country has developed a sustainable path for its energy supply. Awareness of saving energy has been promoted among citizens to increase the use of solar, wind, biomass, waste, and hydropower energies. It is evident that clean energy is less harmful and often cheaper. India is aiming to attain 175 GW of renewable energy which would consist of 100 GW from solar energy, 10 GW from bio-power, 60 GW from wind power, and 5 GW from small hydropower plants by the year 2022 [11]. Investors have promised to achieve more than 270 GW, which is significantly above the ambitious targets. The promises are as follows: 58 GW by foreign companies, 191 GW by private companies, 18 GW by private sectors, and 5 GW by the Indian Railways [12]. Recent estimates show that in 2047, solar potential will be more than 750 GW and wind potential will be 410 GW [13, 14]. To reach the ambitious targets of generating 175 GW of renewable energy by 2022, it is essential that the government creates 330,000 new jobs and livelihood opportunities [15, 16].

A mixture of push policies and pull mechanisms, accompanied by particular strategies should promote the development of renewable energy technologies. Advancement in technology, proper regulatory policies [17], tax deduction, and attempts in efficiency enhancement due to research and development (R&D) [18] are some of the pathways to conservation of energy and environment that should guarantee that renewable resource bases are used in a cost-effective and quick manner. Hence, strategies to promote investment opportunities in the renewable energy sector along with jobs for the unskilled workers, technicians, and contractors are discussed. This article also manifests technological and financial initiatives [19], policy and regulatory framework, as well as training and educational initiatives [20, 21] launched by the government for the growth and development of renewable energy sources. The development of renewable technology has encountered explicit obstacles, and thus, there is a need to discuss these barriers. Additionally, it is also vital to discover possible solutions to overcome these barriers, and hence, proper recommendations have been suggested for the steady growth of renewable power [22,23,24]. Given the enormous potential of renewables in the country, coherent policy measures and an investor-friendly administration might be the key drivers for India to become a global leader in clean and green energy.

Projection of global primary energy consumption

An energy source is a necessary element of socio-economic development. The increasing economic growth of developing nations in the last decades has caused an accelerated increase in energy consumption. This trend is anticipated to grow [25]. A prediction of future power consumption is essential for the investigation of adequate environmental and economic policies [26]. Likewise, an outlook to future power consumption helps to determine future investments in renewable energy. Energy supply and security have not only increased the essential issues for the development of human society but also for their global political and economic patterns [27]. Hence, international comparisons are helpful to identify past, present, and future power consumption.

Table 1 shows the primary energy consumption of the world, based on the BP Energy Outlook 2018 reports. In 2016, India’s overall energy consumption was 724 million tons of oil equivalent (Mtoe) and is expected to rise to 1921 Mtoe by 2040 with an average growth rate of 4.2% per annum. Energy consumption of various major countries comprises commercially traded fuels and modern renewables used to produce power. In 2016, India was the fourth largest energy consumer in the world after China, the USA, and the Organization for economic co-operation and development (OECD) in Europe [29].

Estimated renewable energy potential in India

The estimated potential of wind power in the country during 1995 [37] was found to be 20,000 MW (20 GW), solar energy was 5 × 10 15 kWh/pa, bioenergy was 17,000 MW, bagasse cogeneration was 8000 MW, and small hydropower was 10,000 MW. For 2006, the renewable potential was estimated as 85,000 MW with wind 4500 MW, solar 35 MW, biomass/bioenergy 25,000 MW, and small hydropower of 15,000 MW [38]. According to the annual report of the Ministry of New and Renewable Energy (MNRE) for 2017–2018, the estimated potential of wind power was 302.251 GW (at 100-m mast height), of small hydropower 19.749 GW, biomass power 17.536 GW, bagasse cogeneration 5 GW, waste to energy (WTE) 2.554 GW, and solar 748.990 GW. The estimated total renewable potential amounted to 1096.080 GW [39] assuming 3% wasteland, which is shown in Table 7. India is a tropical country and receives significant radiation, and hence the solar potential is very high [40,41,42].

Gross installed capacity of renewable energy—state wise

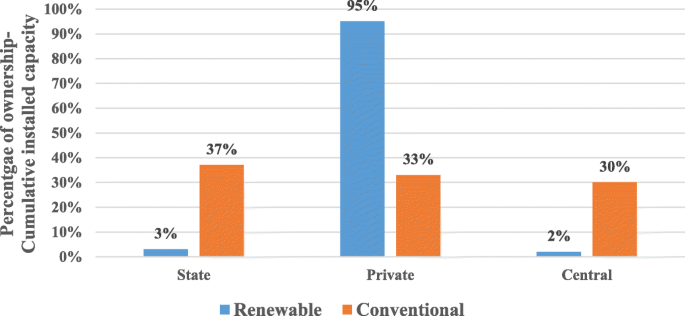

Table 10 shows the installed capacity of cumulative renewable energy (state wise), out of the total installed capacity of 74,081.66 MW, where Karnataka ranks first with 12,953.24 MW (17.485%), Tamilnadu second with 11,934.38 MW (16%), Maharashtra third with 9283.78 MW (12.532%), Gujarat fourth with 10.641 MW (10.641%), and Rajasthan fifth with 7573.86 MW (10.224%). These five states cover almost 66.991% of the installed capacity of total renewable. Other prominent states are Andhra Pradesh (9.829%), Madhya Pradesh (5.819%), Telangana (5.137%), and Uttar Pradesh (3.879%). These nine states cover almost 91.655%.

Solar energy

Under the National Solar Mission, the MNRE has updated the objective of grid-connected solar power projects from 20 GW by the year 2021–2022 to 100 GW by the year 2021–2022. In 2008–2009, it reached just 6 MW. The “Made in India” initiative to promote domestic manufacturing supported this great height in solar installation capacity. Currently, India has the fifth highest solar installed capacity worldwide. By the 31st of December 2018, solar energy had achieved 25,212.26 MW against the target of 2022, and a further 22.8 GW of capacity has been tendered out or is under current implementation. MNRE is preparing to bid out the remaining solar energy capacity every year for the periods 2018–2019 and 2019–2020 so that bidding may contribute with 100 GW capacity additions by March 2020. In this way, 2 years for the completion of projects would remain. Tariffs will be determined through the competitive bidding process (reverse e-auction) to bring down tariffs significantly. The lowest solar tariff was identified to be INR 2.44 per kWh in July 2018. In 2010, solar tariffs amounted to INR 18 per kWh. Over 100,000 lakh (10,000 million) acres of land had been classified for several planned solar parks, out of which over 75,000 acres had been obtained. As of November 2018, 47 solar parks of a total capacity of 26,694 MW were established. The aggregate capacity of 4195 MW of solar projects has been commissioned inside various solar parks (floating solar power). Table 18 shows the capacity addition compared to the target. It indicates that capacity addition increased exponentially.

Table 36 Bioenergy job classification based on education levels

Table 37 Small hydropower job classification based on education levels

The jobs in renewables are categorized into technological development, installation/de-installation, operation, and maintenance. Tables 34, 35, 36, and 37 show the wind industry, solar energy, biomass, and small hydro-related jobs in project development, component manufacturing, construction, operations, and education, training, and research. As technology quickly evolves, workers in all areas need to update their skills through continuing training/education or job training, and in several cases could benefit from professional certification. The advantages of moving to renewable energy are evident, and for this reason, the governments are responding positively toward the transformation to clean energy. Renewable energy can be described as the country’s next employment boom. Renewable energy job opportunities can transform rural economy [79, 80]. The renewable energy sector might help to reduce poverty by creating better employment. For example, wind power is looking for specialists in manufacturing, project development, and construction and turbine installation as well as financial services, transportation and logistics, and maintenance and operations.

The government is building more renewable energy power plants that will require a workforce. The increasing investments in the renewable energy sector have the potential to provide more jobs than any other fossil fuel industry. Local businesses and renewable sectors will benefit from this change, as income will increase significantly. Many jobs in this sector will contribute to fixed salaries, healthcare benefits, and skill-building opportunities for unskilled and semi-skilled workers. A range of skilled and unskilled jobs are included in all renewable energy technologies, even though most of the positions in the renewable energy industry demand a skilled workforce. The renewable sector employs semi-skilled and unskilled labor in the construction, operations, and maintenance after proper training. Unskilled labor is employed as truck drivers, guards, cleaning, and maintenance. Semi-skilled labor is used to take regular readings from displays. A lack of consistent data on the potential employment impact of renewables expansion makes it particularly hard to assess the quantity of skilled, semi-skilled, and unskilled personnel that might be needed.

Key findings in renewable energy employment

The findings comprise (a) that the majority of employment in the renewable sector is contract based, and that employees do not benefit from permanent jobs or security. (b) Continuous work in the industry has the potential to decrease poverty. (c) Most poor citizens encounter obstacles to entry-level training and the employment market due to lack of awareness about the jobs and the requirements. (d) Few renewable programs incorporate developing ownership opportunities for the citizens and the incorporation of women in the sector. (e) The inadequacy of data makes it challenging to build relationships between employment in renewable energy and poverty mitigation.

Recommendations for renewable energy employment

- When building the capacity, focus on poor people and individuals to empower them with training in operation and maintenance.

- Develop and offer training programs for citizens with minimal education and training, who do not fit current programs, which restrict them from working in renewable areas.

- Include women in the renewable workforce by providing localized training.

- Establish connections between training institutes and renewable power companies to guarantee that (a) trained workers are placed in appropriate positions during and after the completion of the training program and (b) training programs match the requirements of the renewable sector.

- Poverty impact assessments might be embedded in program design to know how programs motivate poverty reduction, whether and how they influence the community.

- Allow people to have a sense of ownership in renewable projects because this could contribute to the growth of the sector.

- The details of the job being offered (part time, full time, contract-based), the levels of required skills for the job (skilled, semi-skilled and unskilled), the socio-economic status of the employee data need to be collected for further analysis.

- Conduct investigations, assisted by field surveys, to learn about the influence of renewable energy jobs on poverty mitigation and differences in the standard of living.

Challenges faced by renewable energy in India

The MNRE has been taking dedicated measures for improving the renewable sector, and its efforts have been satisfactory in recognizing various obstacles.

Policy and regulatory obstacles

- A comprehensive policy statement (regulatory framework) is not available in the renewable sector. When there is a requirement to promote the growth of particular renewable energy technologies, policies might be declared that do not match with the plans for the development of renewable energy.

- The regulatory framework and procedures are different for every state because they define the respective RPOs (Renewable Purchase Obligations) and this creates a higher risk of investments in this sector. Additionally, the policies are applicable for just 5 years, and the generated risk for investments in this sector is apparent. The biomass sector does not have an established framework.

- Incentive accelerated depreciation (AD) is provided to wind developers and is evident in developing India’s wind-producing capacity. Wind projects installed more than 10 years ago show that they are not optimally maintained. Many owners of the asset have built with little motivation for tax benefits only. The policy framework does not require the maintenance of the wind projects after the tax advantages have been claimed. There is no control over the equipment suppliers because they undertake all wind power plant development activities such as commissioning, operation, and maintenance. Suppliers make the buyers pay a premium and increase the equipment cost, which brings burden to the buyer.

- Furthermore, ready-made projects are sold to buyers. The buyers are susceptible to this trap to save income tax. Foreign investors hesitate to invest because they are exempted from the income tax.

- Every state has different regulatory policy and framework definitions of an RPO. The RPO percentage specified in the regulatory framework for various renewable sources is not precise.

- RPO allows the SERCs and certain private firms to procure only a part of their power demands from renewable sources.

- RPO is not imposed on open access (OA) and captive consumers in all states except three.

- RPO targets and obligations are not clear, and the RPO compliance cell has just started on 22.05.2018 to collect the monthly reports on compliance and deal with non-compliance issues with appropriate authorities.

- Penalty mechanisms are not specified and only two states in India (Maharashtra and Rajasthan) have some form of penalty mechanisms.

- RPO targets and obligations are not clear, and the RPO compliance cell has just started on 22.05.2018 to collect the monthly reports on compliance and deal with non-compliance issues with appropriate authorities.

- Penalty mechanisms are not specified and only two states in India (Maharashtra and Rajasthan) have some form of penalty mechanisms.

- RPO targets and obligations are not clear, and the RPO compliance cell has just started on 22.05.2018 to collect the monthly reports on compliance and deal with non-compliance issues with appropriate authorities.

- Penalty mechanisms are not specified and only two states in India (Maharashtra and Rajasthan) have some form of penalty mechanisms.

- The parameter to determine the tariff is not transparent in the regulatory framework and many SRECs have established a tariff for limited periods. The FiT is valid for only 5 years, and this affects the bankability of the project.

- Many SERCs have not decided on adopting the CERC tariff that is mentioned in CERCs regulations that deal with terms and conditions for tariff determinations. The SERCs have considered the plant load factor (PLF) because it varies across regions and locations as well as particular technology. The current framework does not fit to these issues.

- Third party sale (TPS) is not allowed because renewable generators are not allowed to sell power to commercial consumers. They have to sell only to industrial consumers. The industrial consumers have a low tariff and commercial consumers have a high tariff, and SRCS do not allow OA. This stops the profit for the developers and investors.

Institutional obstacles

- Institutes, agencies stakeholders who work under the conditions of the MNRE show poor inter-institutional coordination. The progress in renewable energy development is limited by this lack of cooperation, coordination, and delays. The delay in implementing policies due to poor coordination, decrease the interest of investors to invest in this sector.

- The single window project approval and clearance system is not very useful and not stable because it delays the receiving of clearances for the projects ends in the levy of a penalty on the project developer.

- Pre-feasibility reports prepared by concerned states have some deficiency, and this may affect the small developers, i.e., the local developers, who are willing to execute renewable projects.

- The workforce in institutes, agencies, and ministries is not sufficient in numbers.

- Proper or well-established research centers are not available for the development of renewable infrastructure.

- Customer care centers to guide developers regarding renewable projects are not available.

- Standards and quality control orders have been issued recently in 2018 and 2019 only, and there are insufficient institutions and laboratories to give standards/certification and validate the quality and suitability of using renewable technology.

Financial and fiscal obstacles

- There are a few budgetary constraints such as fund allocation, and budgets that are not released on time to fulfill the requirement of developing the renewable sector.

- The initial unit capital costs of renewable projects are very high compared to fossil fuels, and this leads to financing challenges and initial burden.

- There are uncertainties related to the assessment of resources, lack of technology awareness, and high-risk perceptions which lead to financial barriers for the developers.

- The subsidies and incentives are not transparent, and the ministry might reconsider subsidies for renewable energy because there was a sharp fall in tariffs in 2018.

- Power purchase agreements (PPA) signed between the power purchaser and power generators on pre-determined fixed tariffs are higher than the current bids (Economic survey 2017–2018 and union budget on the 01.02.2019). For example, solar power tariff dropped to 2.44 INR (0. 04 USD) per unit in May 2017, wind power INR 3.46 per unit in February 2017, and 2.64 INR per unit in October 2017.

- Investors feel that there is a risk in the renewable sector as this sector has lower gross returns even though these returns are relatively high within the market standards.

- There are not many developers who are interested in renewable projects. While newly established developers (small and local developers) do not have much of an institutional track record or financial input, which are needed to develop the project (high capital cost). Even moneylenders consider it risky and are not ready to provide funding. Moneylenders look exclusively for contractors who have much experience in construction, well-established suppliers with proven equipment and operators who have more experience.

- If the performance of renewable projects, which show low-performance, faces financial obstacles, they risks the lack of funding of renewable projects.

- Financial institutions such as government banks or private banks do not have much understanding or expertise in renewable energy projects, and this imposes financial barriers to the projects.

- Delay in payment by the SERCs to the developers imposes debt burden on the small and local developers because moneylenders always work with credit enhancement mechanisms or guarantee bonds signed between moneylenders and the developers.

Market obstacles

- Subsidies are adequately provided to conventional fossil fuels, sending the wrong impression that power from conventional fuels is of a higher priority than that from renewables (unfair structure of subsidies)

- There are four renewable markets in India, the government market (providing budgetary support to projects and purchase the output of the project), the government-driven market (provide budgetary support or fiscal incentives to promote renewable energy), the loan market (taking loan to finance renewable based applications), and the cash market (buying renewable-based applications to meet personal energy needs by individuals). There is an inadequacy in promoting the loan market and cash market in India.

- The biomass market is facing a demand-supply gap which results in a continuous and dramatic increase in biomass prices because the biomass supply is unreliable (and, as there is no organized market for fuel), and the price fluctuations are very high. The type of biomass is not the same in all the states of India, and therefore demand and price elasticity is high for biomass.

- Renewable power was calculated based on cost-plus methods (adding direct material cost, direct labor cost, and product overhead cost). This does not include environmental cost and shields the ecological benefits of clean and green energy.

- There is an inadequate evacuation infrastructure and insufficient integration of the grid, which affects the renewable projects. SERCs are not able to use all generated power to meet the needs because of the non-availability of a proper evacuation infrastructure. This has an impact on the project, and the SERCs are forced to buy expensive power from neighbor states to fulfill needs.

- Extending transmission lines is not possible/not economical for small size projects, and the seasonality of generation from such projects affect the market.

- There are few limitations in overall transmission plans, distribution CapEx plans, and distribution licenses for renewable power. Power evacuation infrastructure for renewable energy is not included in the plans.

- Even though there is an increase in capacity for the commercially deployed renewable energy technology, there is no decline in capital cost. This cost of power also remains high. The capital cost quoted by the developers and providers of equipment is too high due to exports of machinery, inadequate built up capacity, and cartelization of equipment suppliers (suppliers join together to control prices and limit competition).

- There is no adequate supply of land, for wind, solar, and solar thermal power plants, which lead to poor capacity addition in many states.

Technological obstacles

- Every installation of a renewable project contributes to complex risk challenges from environmental uncertainties, natural disasters, planning, equipment failure, and profit loss.

- MNRE issued the standardization of renewable energy projects policy on the 11th of December 2017 (testing, standardization, and certification). They are still at an elementary level as compared to international practices. Quality assurance processes are still under starting conditions. Each success in renewable energy is based on concrete action plans for standards, testing and certification of performance.

- The quality and reliability of manufactured components, imported equipment, and subsystems is essential, and hence quality infrastructure should be established. There is no clear document related to testing laboratories, referral institutes, review mechanism, inspection, and monitoring.

- There are not many R&D centers for renewables. Methods to reduce the subsidies and invest in R&D lagging; manufacturing facilities are just replicating the already available technologies. The country is dependent on international suppliers for equipment and technology. Spare parts are not manufactured locally and hence they are scarce.

Awareness, education, and training obstacles

- There is an unavailability of appropriately skilled human resources in the renewable energy sector. Furthermore, it faces an acute workforce shortage.

- After installation of renewable project/applications by the suppliers, there is no proper follow-up or assistance for the workers in the project to perform maintenance. Likewise, there are not enough trained and skilled persons for demonstrating, training, operation, and maintenance of the plant.

- There is inadequate knowledge in renewables, and no awareness programs are available to the general public. The lack of awareness about the technologies is a significant obstacle in acquiring vast land for constructing the renewable plant. Moreover, people using agriculture lands are not prepared to give their land to construct power plants because most Indians cultivate plants.

- The renewable sector depends on the climate, and this varying climate also imposes less popularity of renewables among the people.

- The per capita income is low, and the people consider that the cost of renewables might be high and they might not be able to use renewables.

- The storage system increases the cost of renewables, and people believe it too costly and are not ready to use them.

- The environmental benefits of renewable technologies are not clearly understood by the people and negative perceptions are making renewable technologies less prevalent among them.

Environmental obstacles

- A single wind turbine does not occupy much space, but many turbines are placed five to ten rotor diameters from each other, and this occupies more area, which include roads and transmission lines.

- In the field of offshore wind, the turbines and blades are bigger than onshore wind turbines, and they require a substantial amount of space. Offshore installations affect ocean activities (fishing, sand extraction, gravel extraction, oil extraction, gas extraction, aquaculture, and navigation). Furthermore, they affect fish and other marine wildlife.

- Wind turbines influence wildlife (birds and bats) because of the collisions with them and due to air pressure changes caused by wind turbines and habitat disruption. Making wind turbines motionless during times of low wind can protect birds and bats but is not practiced.

- Sound (aerodynamic, mechanical) and visual impacts are associated with wind turbines. There is poor practice by the wind turbine developers regarding public concerns. Furthermore, there are imperfections in surfaces and sound—absorbent material which decrease the noise from turbines. The shadow flicker effect is not taken as severe environmental impact by the developers.

- Sometimes wind turbine material production, transportation of materials, on-site construction, assembling, operation, maintenance, dismantlement, and decommissioning may be associated with global warming, and there is a lag in this consideration.

- Large utility-scale solar plants require vast lands that increase the risk of land degradation and loss of habitat.

- The PV cell manufacturing process includes hazardous chemicals such as 1-1-1 Trichloroethene, HCL, H2SO4, N2, NF, and acetone. Workers face risks resulting from inhaling silicon dust. The manufacturing wastes are not disposed of properly. Proper precautions during usage of thin-film PV cells, which contain cadmium—telluride, gallium arsenide, and copper-indium-gallium-diselenide are missing. These materials create severe public health threats and environmental threats.

- Hydroelectric power turbine blades kill aquatic ecosystems (fish and other organisms). Moreover, algae and other aquatic weeds are not controlled through manual harvesting or by introducing fish that can eat these plants.

Discussion and recommendations based on the research

Policy and regulation advancements

- The MNRE should provide a comprehensive action plan or policy for the promotion of the renewable sector in its regulatory framework for renewables energy. The action plan can be prepared in consultation with SERCs of the country within a fixed timeframe and execution of the policy/action plan.

- The central and state government should include a “Must run status” in their policy and follow it strictly to make use of renewable power.

- A national merit order list for renewable electricity generation will reduce power cost for the consumers. Such a merit order list will help in ranking sources of renewable energy in an ascending order of price and will provide power at a lower cost to each distribution company (DISCOM). The MNRE should include that principle in its framework and ensure that SERCs includes it in their regulatory framework as well.

- SERCs might be allowed to remove policies and regulatory uncertainty surrounding renewable energy. SERCs might be allowed to identify the thrust areas of their renewable energy development.

- There should be strong initiatives from municipality (local level) approvals for renewable energy-based projects.

- Higher market penetration is conceivable only if their suitable codes and standards are adopted and implemented. MNRE should guide minimum performance standards, which incorporate reliability, durability, and performance.

- A well-established renewable energy certificates (REC) policy might contribute to an efficient funding mechanism for renewable energy projects. It is necessary for the government to look at developing the REC ecosystem.

- The regulatory administration around the RPO needs to be upgraded with a more efficient “carrot and stick” mechanism for obligated entities. A regulatory mechanism that both remunerations compliance and penalizes for non-compliance may likely produce better results.

- RECs in India should only be traded on exchange. Over-the-counter (OTC) or off-exchange trading will potentially allow greater participation in the market. A REC forward curve will provide further price determination to the market participants.

- The policymakers should look at developing and building the REC market.

- Most states have defined RPO targets. Still, due to the absence of implemented RPO regulations and the inadequacy of penalties when obligations are not satisfied, several of the state DISCOMs are not complying completely with their RPO targets. It is necessary that all states adhere to the RPO targets set by respective SERCs.

- The government should address the issues such as DISCOM financials, must-run status, problems of transmission and evacuation, on-time payments and payment guarantees, and deemed generation benefits.

- Proper incentives should be devised to support utilities to obtain power over and above the RPO mandated by the SERC.

- The tariff orders/FiTs must be consistent and not restricted for a few years.

Transmission requirements

- The developers are worried that transmission facilities are not keeping pace with the power generation. Bays at the nearest substations are occupied, and transmission lines are already carrying their full capacity. This is due to the lack of coordination between MNRE and the Power Grid Corporation of India (PGCIL) and CEA. Solar Corporation of India (SECI) is holding auctions for both wind and solar projects without making sure that enough evacuation facilities are available. There is an urgent need to make evacuation plans.

- The solution is to develop numerous substations and transmission lines, but the process will take considerably longer time than the currently under-construction projects take to get finished.

- In 2017–2018, transmission lines were installed under the green energy corridor project by the PGCIL, with 1900 circuit km targeted in 2018–2019. The implementation of the green energy corridor project explicitly meant to connect renewable energy plants to the national grid. The budget allocation of INR 6 billion for 2018–2019 should be increased to higher values.

- The mismatch between MNRE and PGCIL, which are responsible for inter-state transmission, should be rectified.

- State transmission units (STUs) are responsible for the transmission inside the states, and their fund requirements to cover the evacuation and transmission infrastructure for renewable energy should be fulfilled. Moreover, STUs should be penalized if they fail to fulfill their responsibilities.

- The coordination and consultation between the developers (the nodal agency responsible for the development of renewable energy) and STUs should be healthy.

Financing the renewable sector

- The government should provide enough budget for the clean energy sector. China’s annual budget for renewables is 128 times higher than India’s. In 2017, China spent USD 126.6 billion (INR 9 lakh crore) compared to India’s USD 10.9 billion (INR 75500 crore). In 2018, budget allocations for grid interactive wind and solar have increased but it is not sufficient to meet the renewable target.

- The government should concentrate on R&D and provide a surplus fund for R&D. In 2017, the budget allotted was an INR 445 crore, which was reduced to an INR 272.85 crore in 2016. In 2017–2018, the initial allocation was an INR 144 crore that was reduced to an INR 81 crore during the revised estimates. Even the reduced amounts could not be fully used, there is an urgent demand for regular monitoring of R&D and the budget allocation.

- The Goods and Service Tax (GST) that was introduced in 2017 worsened the industry performance and has led to an increase in costs and poses a threat to the viability of the ongoing projects, ultimately hampering the target achievement. These GST issues need to be addressed.

- Including the renewable sector as a priority sector would increase the availability of credit and lead to a more substantial participation by commercial banks.

- Mandating the provident funds and insurance companies to invest the fixed percentage of their portfolio into the renewable energy sector.

- Banks should allow an interest rebate on housing loans if the owner is installing renewable applications such as solar lights, solar water heaters, and PV panels in his house. This will encourage people to use renewable energy. Furthermore, income tax rebates also can be given to individuals if they are implementing renewable energy applications.

Improvement in manufacturing/technology

- The country should move to domestic manufacturing. It imports 90% of its solar cell and module requirements from Malaysia, China, and Taiwan, so it is essential to build a robust domestic manufacturing basis.

- India will provide “safeguard duty” for merely 2 years, and this is not adequate to build a strong manufacturing basis that can compete with the global market. Moreover, safeguard duty would work only if India had a larger existing domestic manufacturing base.

- The government should reconsider the safeguard duty. Many foreign companies desiring to set up joint ventures in India provide only a lukewarm response because the given order in its current form presents inadequate safeguards.

- There are incremental developments in technology at regular periods, which need capital, and the country should discover a way to handle these factors.

- To make use of the vast estimated renewable potential in India, the R&D capability should be upgraded to solve critical problems in the clean energy sector.

- A comprehensive policy for manufacturing should be established. This would support capital cost reduction and be marketed on a global scale.

- The country should initiate an industry-academia partnership, which might promote innovative R&D and support leading-edge clean power solutions to protect the globe for future generations.

- Encourage the transfer of ideas between industry, academia, and policymakers from around the world to develop accelerated adoption of renewable power.

Awareness about renewables

- Social recognition of renewable energy is still not very promising in urban India. Awareness is the crucial factor for the uniform and broad use of renewable energy. Information about renewable technology and their environmental benefits should reach society.

- The government should regularly organize awareness programs throughout the country, especially in villages and remote locations such as the islands.

- The government should open more educational/research organizations, which will help in spreading knowledge of renewable technology in society.

- People should regularly be trained with regard to new techniques that would be beneficial for the community.

- Sufficient agencies should be available to sell renewable products and serve for technical support during installation and maintenance.

- Development of the capabilities of unskilled and semiskilled workers and policy interventions are required related to employment opportunities.

- An increase in the number of qualified/trained personnel might immediately support the process of installations of renewables.

- Renewable energy employers prefer to train employees they recruit because they understand that education institutes fail to give the needed and appropriate skills. The training institutes should rectify this issue. Severe trained human resources shortages should be eliminated.

- Upgrading the ability of the existing workforce and training of new professionals is essential to achieve the renewable goal.

Hybrid utilization of renewables

- The country should focus on hybrid power projects for an effective use of transmission infrastructure and land.

- India should consider battery storage in hybrid projects, which support optimizing the production and the power at competitive prices as well as a decrease of variability.

- Formulate mandatory standards and regulations for hybrid systems, which are lagging in the newly announced policies (wind-solar hybrid policy on 14.05.2018).

- The hybridization of two or more renewable systems along with the conventional power source battery storage can increase the performance of renewable technologies.

- Issues related to sizing and storage capacity should be considered because they are key to the economic viability of the system.

- Fiscal and financial incentives available for hybrid projects should be increased.

Conclusion

The renewable sector suffers notable obstacles. Some of them are inherent in every renewable technology; others are the outcome of a skewed regulative structure and marketplace. The absence of comprehensive policies and regulation frameworks prevent the adoption of renewable technologies. The renewable energy market requires explicit policies and legal procedures to enhance the attention of investors. There is a delay in the authorization of private sector projects because of a lack of clear policies. The country should take measures to attract private investors. Inadequate technology and the absence of infrastructure required to establish renewable technologies should be overcome by R&D. The government should allow more funds to support research and innovation activities in this sector. There are insufficiently competent personnel to train, demonstrate, maintain, and operate renewable energy structures and therefore, the institutions should be proactive in preparing the workforce. Imported equipment is costly compared to that of locally manufactured; therefore, generation of renewable energy becomes expensive and even unaffordable. Hence, to decrease the cost of renewable products, the country should become involve in the manufacturing of renewable products. Another significant infrastructural obstacle to the development of renewable energy technologies is unreliable connectivity to the grid. As a consequence, many investors lose their faith in renewable energy technologies and are not ready to invest in them for fear of failing. India should work on transmission and evacuation plans.

Inadequate servicing and maintenance of facilities and low reliability in technology decreases customer trust in some renewable energy technologies and hence prevent their selection. Adequate skills to repair/service the spare parts/equipment are required to avoid equipment failures that halt the supply of energy. Awareness of renewable energy among communities should be fostered, and a significant focus on their socio-cultural practices should be considered. Governments should support investments in the expansion of renewable energy to speed up the commercialization of such technologies. The Indian government should declare a well-established fiscal assistance plan, such as the provision of credit, deduction on loans, and tariffs. The government should improve regulations making obligations under power purchase agreements (PPAs) statutorily binding to guarantee that all power DISCOMs have PPAs to cover a hundred percent of their RPO obligation. To accomplish a reliable system, it is strongly suggested that renewables must be used in a hybrid configuration of two or more resources along with conventional source and storage devices. Regulatory authorities should formulate the necessary standards and regulations for hybrid systems. Making investments economically possible with effective policies and tax incentives will result in social benefits above and beyond the economic advantages.